IN THE HIGH COURT OF SOUTH AFRICA, FREE STATE DIVISION, BLOEMFONTEIN

Case number: 2769/2017

In the matter between:

HANNES MARTHINUS JONKER First Applicant

HENDRIK PHILLIUS FOURIE LEWIS Second Applicant

JOSEPH IVAN MARKS Third Applicant

SUSARA DEBORAH OBERHOLZER Fourth Applicant

JABULANI PERTROLS MTSWENI Fifth Applicant

GILBERT LOFTUS RATHOKOLO Sixth Applicant

SAMANTHA ANNE TURNER Seventh Applicant

and

LAMBONS (PTY) LTD First Respondent

OSHENE MOROBANE N.O. Second Respondent (In her capacity as Taxing Master of the High Court)

HEARD ON: 13 SEPTEMBER 2018

JUDGMENT BY: DANISO, AJ

DELIVERED ON: 08 NOVEMBER 2018

[1] The applicants were plaintiffs in an action instituted against the first respondent for unpaid salaries. On 22 February 2018 the parties concluded a settlement agreement (Annexure “FA3”) in terms of which the first respondent agreed to pay the amounts due to the applicants and the taxed costs. The agreement was made an order of court on 22 February 2018. That ought to have resolved the issues between the parties but that was not to be.

[2] The taxation of the said costs was set down on 08 May 2018 before the second respondent (the “Taxing Master”). Ms van Deventer an admitted attorney with a right of appearance in the high court enrolled in the Gauteng Division appeared for the applicants whilst Ms Van Wyck appeared for the first respondent. The taxation did not proceed. Van Deventer was prevented from

representing the applicants on the basis that only the attorneys whose names are on the roll of attorneys for this division are allowed to represent a party in the taxation. The taxation was consequently postponed. It is in that regard that the applicants have launched these proceedings seeking to review the taxing master’s ruling. The application is opposed by the first respondent.

[3] In its answering affidavit the first respondent raised three points in limine that: the application is irregular for want of compliance with PAJA, Rule 48 or 53 and also the non-joinder of the Department of Justice in the proceedings.

Non-compliance with PAJA, Uniform Rules of Court, 48 and/or 53

[4] The first respondent contends that the application is irregular as it is neither premised on the Promotion of Administrative Justice Act, Rule 48 or 53. I disagree. The Promotion of Administrative Justice Act (‘PAJA’)1 is a pathway for a judicial review of administrative actions. A taxing master performs a quasi-judicial function and not an administrative function. PAJA is therefore not applicable in these circumstances.

[5]

It is trite that Rule 48 is applicable in a situation where a review is directed at challenging a ruling or rulings made by the taxing master on items in the bill to be taxed and after which the master

made an allocator. The situation presenting itself on the facts of this case is clearly not one envisaged by the Rule. The master did not conduct any taxation, the review is instead directed at her ruling against the appearance of the applicant’s representative at the taxation. Rule 53 does not make its use peremptory for matters which fall within its ambit. It merely facilitates access to the record of the proceedings in which the decision was made and the reasons for that decision. It is there for the benefit of the applicants who are at liberty to enjoy if, and to the extent needed in their particular circumstances. This objection cannot be upheld.

Non-joinder of the Department of Justice

[6] According to the first respondent, the applicants are seeking relief against a decision of the functionary of the Department of Justice in her capacity as such therefore the Department of Justice must also be cited in these proceedings. There is no merit to this objection, the taxing master has the necessary locus standi to be cited in her official capacity as the taxing master.

[7] I therefore hold that the first respondent’s objections are unfounded and they are accordingly dismissed.

[8] I now turn to the issue under review. The issue that arise in this review is the regularity of the taxing master’s decision in

preventing the applicants’ attorney from appearing at the taxation set down before the said taxing master.

[9] It was the applicants’ case that the taxing master’s ruling was based on a misinterpretation or wrong understanding of the provisions of this court’s Practice Directives. The ruling was accordingly wrong. The applicants also launched an attack on the objectivity of the taxing master. It was averred that her behaviour was quite opportunistic in that despite having been adamant that van Deventer was not permitted to appear at the taxation, the taxing master nevertheless suggested that she would allow van Deventer to appear, provided she agreed to waive the right to review the rulings that the taxing master would make at the said taxation.

[10] On the other side, the first’s respondent’s case is one of curious contradiction. Although it was submitted by counsel for the first respondent that the granting of the order is not opposed except for the order relating to costs, the first respondent’s answering affidavit says otherwise. The application is opposed on the preliminary points and also on the merits.

[11] Ultimately it has to be decided whether the taxing master erred or exercised her discretion wrongly in barring the plaintiff’s legal representative from representing the applicants at the taxation.

[12] It is settled law that the court will not interfere with the exercise of the taxing master’s discretion unless it appears that such has not been exercised judicially or it was exercised improperly or wrongly, for example, by disregarding factors which she should have considered, or considering matters which were improper for her to have considered, or she had failed to bring her mind to bear on the question in issue, or she had acted on a wrong principle. The court will however interfere where it is of the opinion that the taxing master was clearly wrong. See Wellworths Bazaars Ltd v Chandler’s LTD 1947 (4) SA 453 (T) 457 to 458.

[13] The issue of a right of appearance before a taxing master was dealt with In Bills of Costs (Pty) Ltd and Another v The Registrar, Cape, NO and Another 1979 (3) SA 925 (A) where it was held that a taxation is an integral part of the judicial process. The rights and obligations of the parties to a suit are not finally determined until the costs ordered by the court have been taxed, accordingly the only persons who can appear before a taxing master in a Supreme Court (now the high court) are persons who are permitted to practise in such court. At that time, the persons who were permitted to practice in the high court were advocates.

[14] The Right of Appearance in Courts Act2 (‘The Act’) was enacted in 1995 to “level the field” between advocates and attorneys by extending the right of attorneys to appear in the high court.

[15] Attorneys who have been granted the right of appearance in the high court are entitled to appear in the high court and to discharge the functions of an advocate in any proceedings in the high court throughout the Republic.3

[16] It was not in dispute that van Deventer is indeed an attorney with a right of appearance in the high court as envisaged in sections 3(4) and 4(4) of the Act. In opposing the application the first respondent relied on the Practice Directives by AJP Rampai (as he then was) and S v Sewnandan 1999 (2) SA 1087 (O).

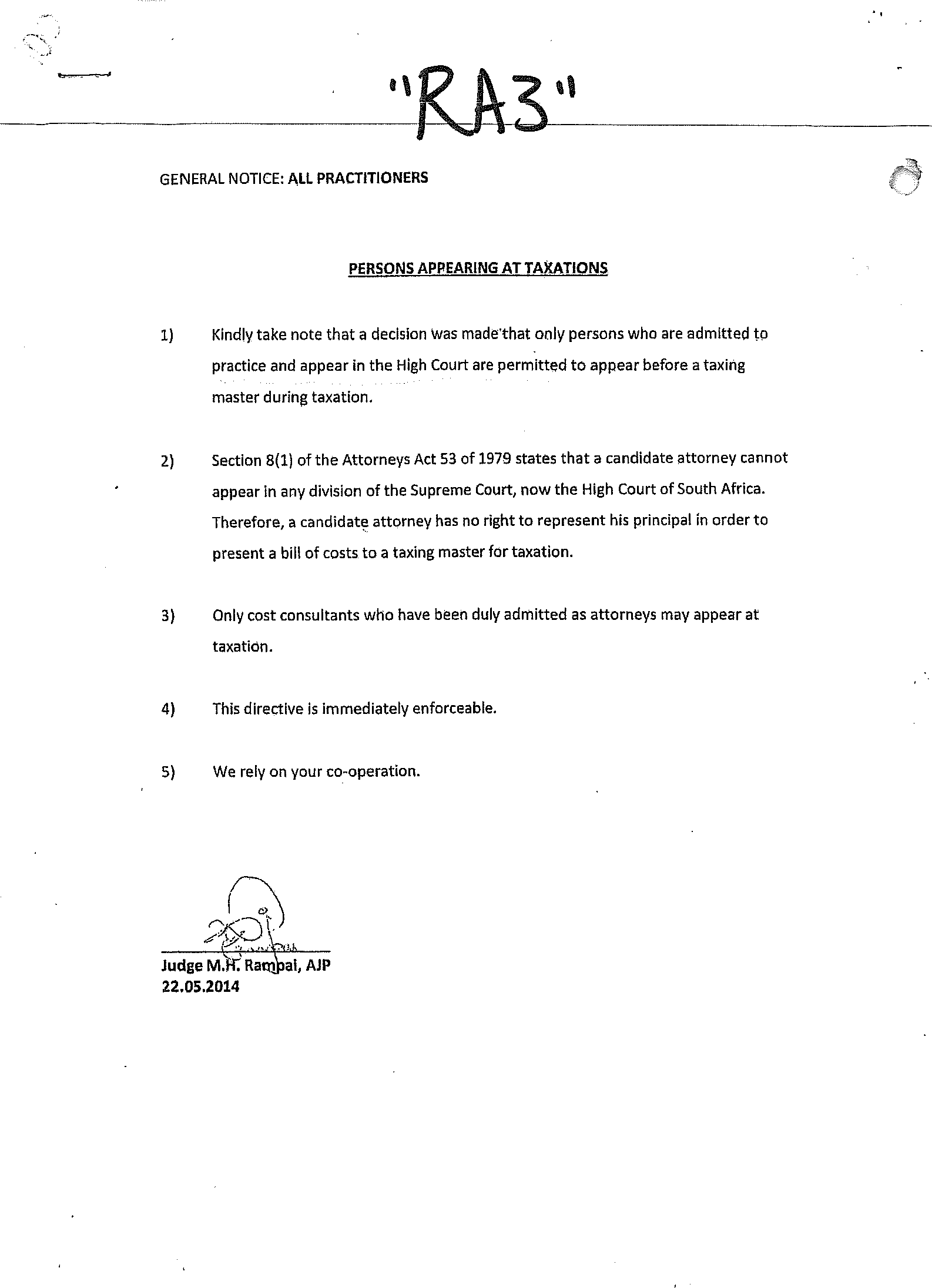

[17] The practice directives of this court merely mimic the dictum in Bills of Costs (Pty) Ltd and Another supra. They do not provide that only attorneys whose names appear on this division’s roll of attorneys may appear at the taxation. See hereunder a copy thereof, Annexure “RA3”, at paragraph 1. The taxing master has clearly misconstrued the practice of this court.

2 Act No. 62 of 1995 (as amended).

3 Section 3(4) and section 4(4) inserted pursuant to the 2005 amendment.

[18] In the Sewnandan’s matter the court found that only the attorneys’ right to appear in the high court had been extended by the Act, the attorney’s area jurisdiction was not extended. The case was decided before the Act was amended by the introduction of section 4(4) in 2005.

[19] I’m of the view that section 4(4) of the Act specifically grants the attorney who has been issued with a certificate of right appearance in terms of section 4(2), a right to appear in all the divisions of the high court to discharge all other functions of an advocate in any proceedings (my emphasis) in those divisions. In my view, “any proceedings” include appearing before a taxing master for taxation.

[20] The Act has not replaced the Attorneys Act (53 of 1979) in that the right to practice4 as an attorney outside the area in which the attorney is enrolled is still regulated by sections 20 and 21 of the said Act.

[21] The taxing master has misconceived the facts and the circumstances as to the practice of this court. Her ruling was clearly wrong.

4 An attorney must be enrolled within a particular division in other to establish a firm and to sign pleadings and notices in that division.

[22] It was common cause that the taxation which is subject to this application is the second taxation involving the same parties. The first taxation was set down on 15 February 2018. The applicants were not satisfied with the taxing master’s rulings and launched a review application. The taxing master’s actions in bargaining with van Deventer that she could represent the applicants in the taxation provided she agrees to waive the right to review the rulings made at the taxation are quiet disturbing and cast doubt to her impartiality. A taxing master performs a function of a judicial nature, her independence and impartiality must be beyond reproach.

[23] Taking into consideration all the facts of this matter, I have come to a conclusion that the taxing master erred in her decision to prevent the applicants’ attorney from appearing at the taxation.

[24] There is no reason why the ordinary rule of costs following the result should not apply. The first respondent’s legal representative was the substantive cause of the irregularity, by incorrectly objecting to the applicants’ appearance at the taxation thus occasioning the wasted costs of 08 May 2018, by effectively postponing the taxation.

[25] For the above reasons, I hereby make the following orders:

1. The ruling of the taxing master in terms of which she prevented the applicants’ attorney from appearing at the taxation is set aside.

2. It is declared that an attorney, who has been issued with a certificate of right appearance in terms of section 4(2) of the Act, is permitted to appear before the taxing master during taxation.

3. The matter is remitted back to the taxing master to proceed with the taxation of the bill of costs, and the ordinary rules pertaining to taxation shall apply.

4. The first respondent is ordered to pay the costs of the review, together with the wasted costs of 08 May 2018 occasioned by the non-taxation of the bill of costs.

5. The Registrar is directed to forward a copy of this judgment to the Judge President pursuant to the remarks made in paragraph [22] above.

NS DANISO, AJ

APPEARANCES:

Counsel on behalf of Applicants: Advocate Ebersohn

Instructed by: Gerrie Ebersohn Attorneys c/o Webber Attorneys BLOEMFONTEIN

Counsel on behalf of First Respondent: Advocate Le Roux Instructed by: Gous Vertue & Ass Inc.

BLOEMFONTEIN